If the Money is Broken, So is the Market

Our last article focused on Broken Money. A functional economy is ever harder to sustain when debt and interest payments keep rising faster than GDP. And the relentless decline of our fiat money system now sits at the front of every wealth management decision.

This week covers the consequences: Broken Markets. If the money is broken, the market built on it is broken too. After the second quarter of 2026, the price behavior shows just how broken the market really is. The time has come to take this seriously.

The Financial System is NOT Designed for Your Benefit

In a fiat money system (government-issued money that is not backed by a physical commodity like gold), there can be no level playing field. Most people are not sufficiently aware of this reality and the multiple mechanisms of market manipulation working against them.

A fiat money system is a managed system, and a managed system is never neutral. The first handlers of newly created money understand its consequences and therefore hold a large advantage over the last handlers. That advantage becomes more egregious as the system deteriorates. This is not a bug; it’s a feature. And it cancels the individual’s capacity for better judgement.

“The people who handle the new government money first buy when product prices are still low… The first handlers gain extra money for some purchases, while the last handlers lose on all purchases. This redistributes wealth… taking money from the freest people, whose connections to the government are the most distant.” — Mises Wire

It is a mistake to assume the financial system is designed for your benefit. You are the last money handler.

If you are not proactive in safeguarding your best interest, you will increasingly pay the price. What follows is an expression of this single fact across every mechanism:

- Increasing Market Concentration

- Destabilization by Leveraged ETFs

- IPOs Manipulating Markets and Changing Rules

- Insider Trading at the Highest Level

- A Retirement System Loaded with Risk at the Worst Possible Moment

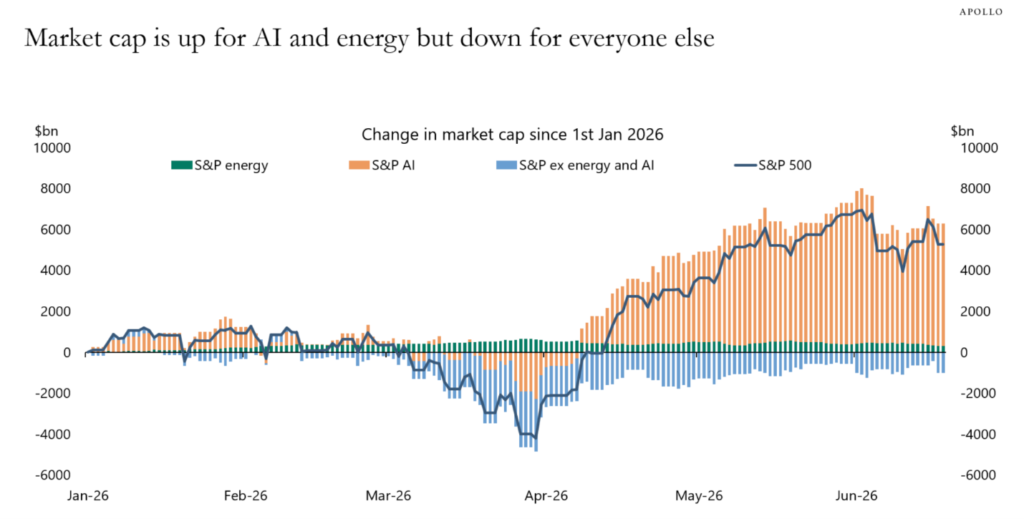

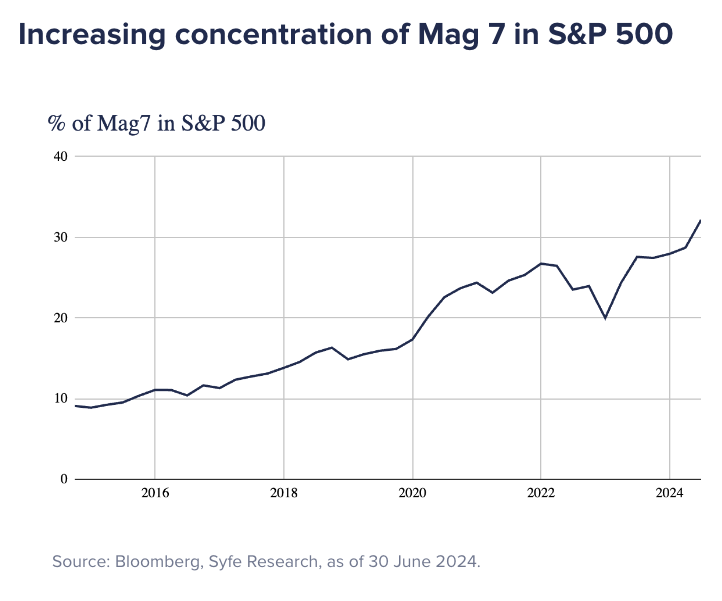

The S&P 500 Has Become a Single Bet on AI

AI stocks have dominated S&P 500 performance this year.

The S&P 500 was supposed to be a broad, balanced representation of the market. That is no longer what it is.

This year it reflects one theme: Artificial Intelligence. This concentration has been building for years. More and more of the index now rests on just seven stocks, the Mag 7 (Magnificent Seven — seven mega-cap tech and growth companies that dominate the U.S. stock market: Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla).

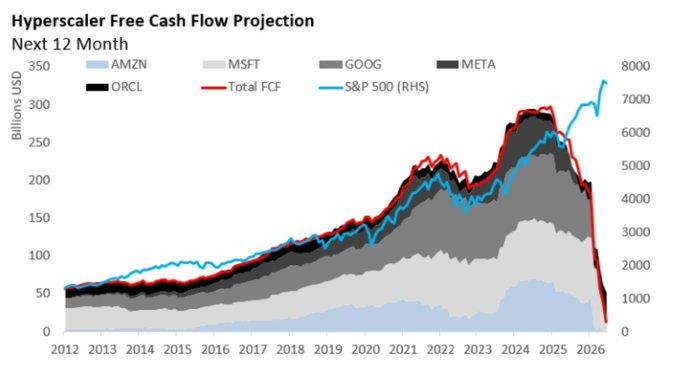

This matters for anyone who treats the S&P 500 as a neutral benchmark. It is no longer a consistent, broad index. Today, holding it is making a “call” on AI. The index was for a long time very highly correlated with hyperscaler free cash flow, and there are signs that correlation is now breaking down.

There are also growing concerns about how quickly AI will actually be adopted. As Bain has noted, “44% of large companies that are funding their next wave of AI spending are basing those investments on the last round of savings — savings that haven’t yet materialized.”

Leveraged ETFs Have Made the Market a Forced Buyer

The concentration is dangerous on its own. Leverage makes it unstable. Leveraged funds are forced buyers: to hold their promised exposure, they must buy more every time the market rises, automatically, regardless of price or value. When enough money piles into them, that forced buying stops following the market and starts driving it.

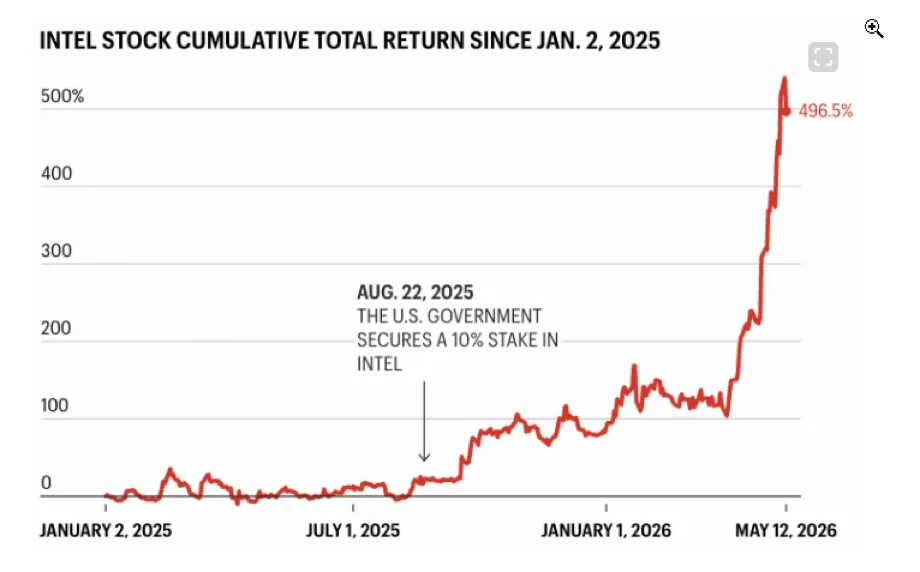

Barclays has flagged extreme concern, with good reason. Leveraged ETFs are, in their words, “the largest non-discretionary driver of risk at present, and having grown orders of magnitude larger already YTD runs the risk of cascading into a more protracted sell off… if not cauterized by an external event.” These vehicles had cumulatively bought almost $300 billion of notional exposure to various single names and indices “now dwarfing any other vertical of systematic risk, be it CTAs, Vol Control, etc., and a somewhat terrifying figure to contend with should it need to be unwound in a short period of time.”

Tier1 Alpha, a leader in flow analysis, has put numbers on it. In a single day, one leveraged product, SOXL, had to buy an estimated $9.1 billion of semiconductors by the close to maintain its 3x leverage — roughly a third of the monthly 401(k) equity flows we would typically expect, from one product, in one day. The top beneficiaries were MU, up over 209% since March 31st, AMD up 164%, and INTC up 165% over the same period.

In their words, these extraordinary gains have not been driven by stronger fundamentals, but by the persistent requirement for leveraged ETFs to buy into momentum. This is a perpetual feedback loop of rebalancing demand that is artificially driving prices higher.

The setup is increasingly dangerous, because the same dynamics that drive prices up can reverse just as fast, with potentially catastrophic consequences for the broader market and the semiconductor sector in particular. Markets may well continue higher in the near term, but the mechanical momentum behind the move is highly unstable.

The Latest Manipulation: SpaceX IPO Headed for Your Account

The most immediate and obvious example is the SpaceX IPO. There are so many problems with this new equity issue that it takes a full breakdown to see them all, which is why the explainer is worth watching.

This matters materially, because the issue will be routed into your investment account whether you choose it or not. The same rule change now channeling private equity into 401(k) target-date funds — which we come to below — is exactly how a pre-IPO holding like SpaceX reaches you. The big ETFs inside 401(k)s become forced buyers of SPCX over time, and it is already happening.

Insider Trading at the Highest Level

Among the most predictive information on a stock is insider activity. Insiders are the most informed participants, and the most likely to hold non-public information. In describing this I make no judgment. I only want to recognise the impact on the market.

Markets have benefitted considerably from a new initiative of government direct stock purchases. Washington’s latest and boldest experiment in industrial policy is a renewed willingness to take equity stakes. Since January 2025, the US government has invested $20.9 billion across sixteen deals involving direct ownership, and it appears to have contributed to the explosive semiconductor rally.

When the activity of insiders becomes known, it becomes a factor in prices, and that is particularly true when the insider is the President, whose trades are public record and include some of the market’s biggest winners. This has further supported confidence in the recent performance of the stock market and of many technology stocks.

Don’t Let Your 401(k) Be the Exit Liquidity

When the biggest bubble in history turns down, every position needs a buyer of last resort. Too often, that buyer is your retirement account.

Investors are not being informed that their portfolio risk is rising dramatically. On some measures, the market now trades at twice the valuation of the dot-com peak. The Buffett Indicator tells the same story.

No one complains in a bull market. But the scale of the dysfunction has gone too far to ignore the risk facing investors who do not understand how quickly that risk is accelerating.

And They’re Adding More Risk, Not Less

It gets worse.

Not only are 401(k) investors not being told their risk is rising, but even more high-risk assets are being added to their accounts.

Many 401(k) administrators already do a poor job, with questionable target-date funds, weak risk assessment, and little information for beneficiaries. There is no excuse for going yet a step further and adding still more high-risk assets.

Yet that is what is happening. Driven by new Department of Labor “safe harbor” guidance and a White House executive order to open private markets to everyday savers, 401(k) plans are now incorporating alternative assets: private equity and venture capital, private credit, crypto, real estate and infrastructure, and commodities.

Rather than offer these as standalone options, large managers such as BlackRock are embedding them directly into target-date funds as “sleeves” running from roughly 5% to 20% of the fund. The least liquid, hardest-to-value assets are being added at what is, on some measures, twice the valuation of the dot-com peak. This is the same channel that can place a holding like SpaceX into your account without you ever choosing it.

The Best Investors Are Already Warning

Broken money and broken markets are exactly what many of the best investors of all time are now warning about.

Keith McCullough, the founder of Hedgeye, has one of the best and most transparent track records I can find.

Ray Dalio is clearly concerned about broken money.

Paul Tudor Jones is clearly concerned about US stocks, and broken markets.

You need to find a way to question the remarkable bullish consensus in US equities at record all-time highs. Before taking any action, conduct an immediate review of how you are invested, and take a balanced, considered view of future prospects. If you would like a personalized consultation, book a call.

Most people have never experienced a fiat currency collapse. They happen only a few times in a century, but every fiat system will collapse eventually. At this stage of deterioration, it is becoming unlikely that the US can avoid a major reset of its currency system. That is a matter of financial survival, not a temporary setback.

The collapse is already underway. The S&P 500 has underperformed gold by 70% since the year 2000. The dollar has fallen 99% against gold since 1971. The process is accelerating. Most investors urgently need a new mindset and framework, because conventional advice has become not only inadequate but dangerous. Do not fall behind any further.

For more like this, subscribe to our Substack. In these increasingly challenging times, we strive to cover the most vital matters with Your Best Interest as the priority.