Why This Question Matters Now

For most Americans, a bank account feels as fundamental as a phone or car. That intuition is exactly what the founders warned us about.

“All the perplexities, confusion and distress in America arise not from defects in the constitution or confederation, nor from want of honor or virtue, as much from downright ignorance of the nature of coin, credit, and circulation.”

— John Adams, in a letter to Thomas Jefferson

Adams isn’t describing a crisis. He’s describing the background condition of what goes wrong when ordinary citizens stop paying attention to the financial system holding their money.

Two centuries later, the consequences have arrived. The US is in an advanced debt crisis. Measured in gold, the dollar has lost over 99% of its value since it was delinked a few decades ago. That wealth destruction has already happened; it just isn’t visible in the units most people are watching. That is what fiat currencies do when banks are permitted to create loans for free and leverage the profits.

You almost certainly need a bank. On-demand deposits, transfers, payments — these services are exclusive by law to chartered banks and similar institutions. The real question, and the one most savers never think to ask, is how much of your financial life should rely on banks?

The answer is: as little as possible.

The good news is that you don’t have to choose. Link your existing bank account to an Ultimate Savings Account, and you keep the banking functions you actually need while mitigating the disadvantages. You also gain access to by far the best savings vehicle available today, at Interactive Brokers.

The Bank-Government Codependency

Banks aren’t just companies. They sit inside a co-dependent relationship with the government, giving them privileges no other kind of business has. The most consequential of these is the right to create money by leveraging their balance sheet.

The mechanics are simple. If a bank can lend at 6% while borrowing at 3%, it earns 3%. Run that same trade with 10x leverage and the bank earns 30%. And every dollar of deposit money lent out doesn’t leave the bank. When a bank makes a loan, it doesn’t typically hand out cash; it credits the borrower with a new deposit.

Picture it this way. Your original account still shows your deposit. Ten new accounts now show ten new deposits, created by ten loans. The bank holds ten profitable loans paying a higher rate than the depositor receives on the original balance. This is enormously profitable. It is also enormously fragile. The bank is leveraged, runs a duration mismatch between short deposits and long loans, and if just two of those ten loans default it is insolvent on the arrangement.

So when the loans go bad, what happens? Either the taxpayer absorbs the loss directly through a bailout, or the government prints the money to do it and the public pays through inflation. In practice the answer has been both, repeatedly.

This is a remarkable privilege. It’s extraordinarily profitable for banks, and it expands the money supply at a pace citizens never consented to and often don’t understand.

The founders saw it coming, which is not surprising given the perfect failure record of financial systems built on this design over thousands of years.

“I sincerely believe… that banking establishments are more dangerous than standing armies.”

— Thomas Jefferson, 1816 letter to John Taylor

Jefferson wasn’t speaking metaphorically. He opposed private banks controlling currency through inflation and deflation because he saw it as a structural threat to both liberty and a stable financial system.

Over time, the rules governing the bank-government relationship change. They typically favor either the banks or the government. Public recourse, your ability as a depositor to push back on policy or service, declines. Power and benefit concentrate at the top, and income inequality rises with it.

This isn’t a story about bad actors. It’s a story about incentives.

In 2008, Merrill Lynch was plainly bankrupt. A month later it was bailed out with taxpayer money, and employees collected their bonuses. Tell me which other companies receive that kind of support when they fail completely.

The fiat system that backs all of this has a long track record, and it isn’t good. By one count, roughly 600 of 775 documented fiat currencies have failed, an 87% failure rate that continues to rise. Average lifespan: 27 to 35 years. The current US dollar has lasted over 50, and counting.

You don’t have to predict the next crisis to act on this. You just have to recognize that the system rewards the people running it and asks the public to absorb the cost.

The Four Risks to Your Deposit Today

Once you accept that the bank is not a neutral utility, four concrete problems with bank deposits become hard to ignore.

1. Your deposit is part of the bank’s capital structure.

The 2010 Dodd-Frank Act introduced bank “bail-in” mechanics in the United States via the Orderly Liquidation Authority. The intent was to avoid taxpayer-funded bailouts. The effect, for depositors, is that uninsured deposits can be written down or converted to equity to recapitalize a failing bank. Put plainly: your deposit is part of the bank’s capital until the bank lets you have it back. A resolution scenario is just when you find out.

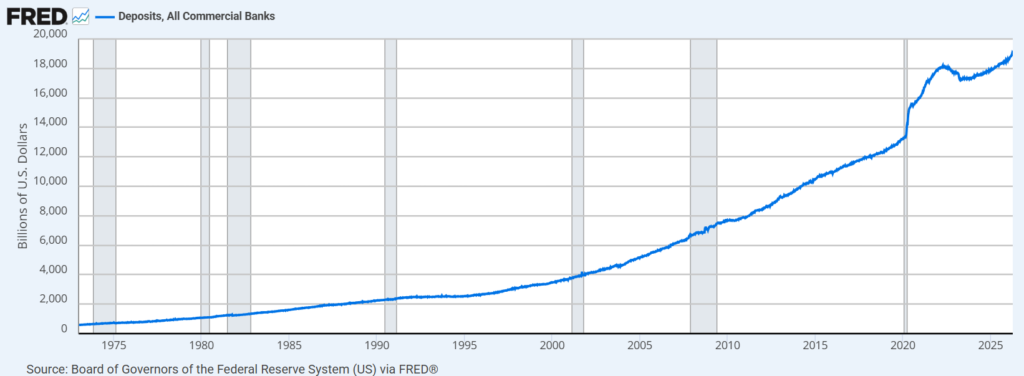

US commercial bank deposits are over $19 trillion, and have been for years. There is no plausible scenario in which that quantity gets bailed out without money printing on a scale that would destroy the dollar’s value. The system isn’t sized for the rescue it implicitly promises.

2. Access can be delayed, scrutinized, or refused.

There are no legal limits on how much you can deposit. But there are extensive rules on what happens when you do.

Under the Bank Secrecy Act, banks must file a Currency Transaction Report for any cash deposit exceeding $10,000 in a single business day, including multiple smaller deposits that aggregate over 24 hours.

Anti-structuring laws prohibit splitting deposits to avoid this threshold. Banks may file Suspicious Activity Reports on patterns below the threshold if they appear designed to evade reporting. Individual banks set their own additional limits: ATM bill caps, mobile deposit ceilings, holds on large or unusual checks.

Even for “on-demand” accounts, access can be delayed and subject to scrutiny.

3. Debanking is an increasing risk.

Individuals and businesses have been “debanked,” with accounts closed without explanation or notice. This isn’t just a legal theory. This is a reality that is becoming increasingly difficult to ignore.

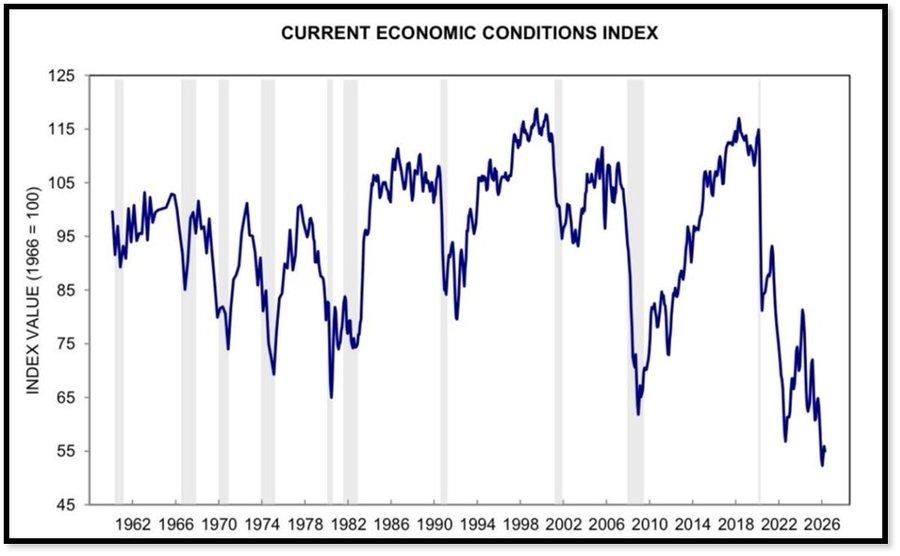

4. The macro environment is working against you.

The first three risks live inside the bank itself. The fourth surrounds it. US consumer confidence sits near multi-decade lows. The economy is more split between rich and poor than at any point in living memory. Growth has been declining for decades. The credit of US government debt has been downgraded. Bank derivative exposure and debt-to-GDP are at record levels. Even highly respected bank analysts, Chris Whalen for example, are openly favoring precious metals as a hedge against the system’s fragility.

You can watch more from Whalen here.

These four risks are not balanced by an offsetting reward. The whole structure asks you to take them on with no compensating yield, no upside, and limited recourse.

The Alternative: a Brokerage as Your Savings Account

The good news is that the transactional services a bank provides — and the savings function people assume comes bundled with them — are now cleanly separable. You can keep the first inside a bank and move the second outside.

The vehicle is a brokerage account at Interactive Brokers (IBKR), linked to your existing bank account.

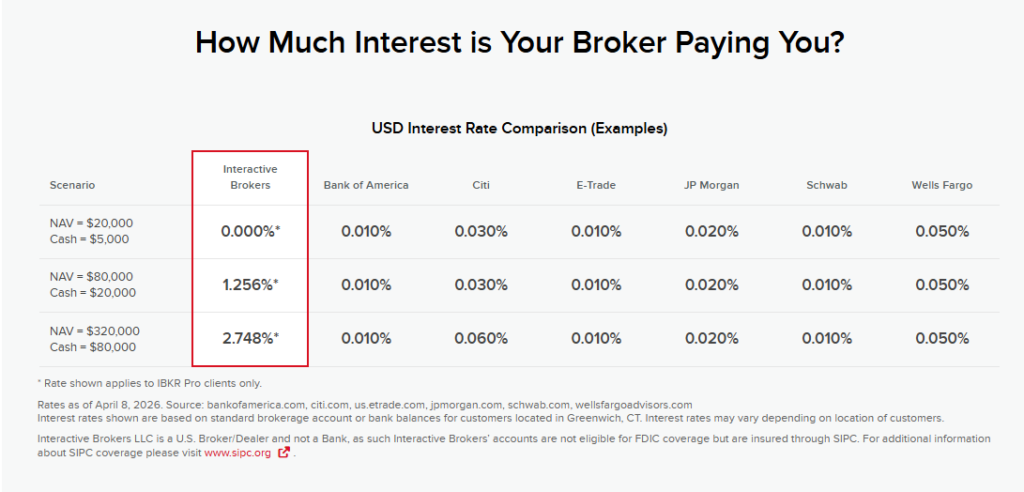

Start with the simplest comparison most people will care about. Here’s the interest a typical broker pays on uninvested cash, side-by-side with the major US banks:

Rates as of April 8, 2026. Source: each institution’s published rates. Interactive Brokers is SIPC-insured (not FDIC).

As the table shows, on any meaningful balance, the interest you receive at IBKR is dramatically higher than at any major US bank. And that edge is yours before you make a single investment decision.

Why IBKR specifically

I’ve used Interactive Brokers for over thirty years. They’re a public company, an S&P 500 component, with real-time disclosure and decades of risk management through every cycle in living memory. Barron’s currently ranks them the top discount broker globally. Brokerage assets are SIPC-insured up to $500,000 — a higher protection level than FDIC’s limit on bank deposits.

The institution itself has a better track record than any US bank. The whole banking system was bankrupt in 2008. IBKR has never had a credit issue anywhere close to that.

What you can do from the same account

Once you have an IBKR account, the menu opens up:

- Treasury Bills for short-duration safety

- Floating Rate Notes for income that adjusts with rates

- Treasury Inflation Protected Securities (TIPS) for purchasing-power protection

- Treasuries at any maturity for fixed income

- The widest access to listed global securities, futures, and options available on any platform

You can either run this yourself or work with an advisor who can show you the track record of running such an account. My background is 42 years in financial markets, including a stint as Managing Director on JP Morgan’s proprietary trading desk in London. That’s the perspective I bring to client portfolios.

Capital in the account can be wired to any major destination in the world at will.

How to Make the Switch

The operational answer is deliberately simple:

- Open an IBKR account. A few clicks online.

- Link it to your existing bank account. One free monthly transfer, in either direction, fully at your initiative.

- Move surplus cash out of the bank. Keep the bank account funded for monthly transactions and bills. Move everything beyond that to IBKR.

- Allocate. Even leaving the cash unmanaged, you’ll earn meaningfully more than your bank pays. Or step into Treasuries, TIPS, or any of the instruments listed above.

The switch itself is small. The decision to make it is the part that actually matters.

The bigger picture

US investors are overdependent on banks and underinvested in everything that protects purchasing power outside the banking system. Don’t expect that diagnosis from a financial advisor affiliated with a bank.

The fix is straightforward. The bank still handles transactions. A brokerage account handles savings, yield, and optionality. That’s the best arrangement available today for your long-term capital, and you don’t need permission from your bank to make it.

Subscribe to the Substack if you would like access to The Ultimate Savings Account Setup Guide as soon as it’s ready.

Cheers,

Chris